Summary

- Resurrect your tried and proven lead generation practices.

- Revisit client relationship and referral strategies.

- Focus on cross-selling and up-selling.

- Refine or rebuild your team.

- Invest in your agency.

- Leverage an insurance network.

When insurance market conditions shift, agencies feel the impact. Right now, the industry shows signs of softening. While this is welcome news for policyholders and the agents who serve them, it also means that the competition is about to heat up. It’s important to stay ahead of the curve by realigning your priorities and practices to keep pace with the evolving landscape.

Improved Capacity and Lower Rates

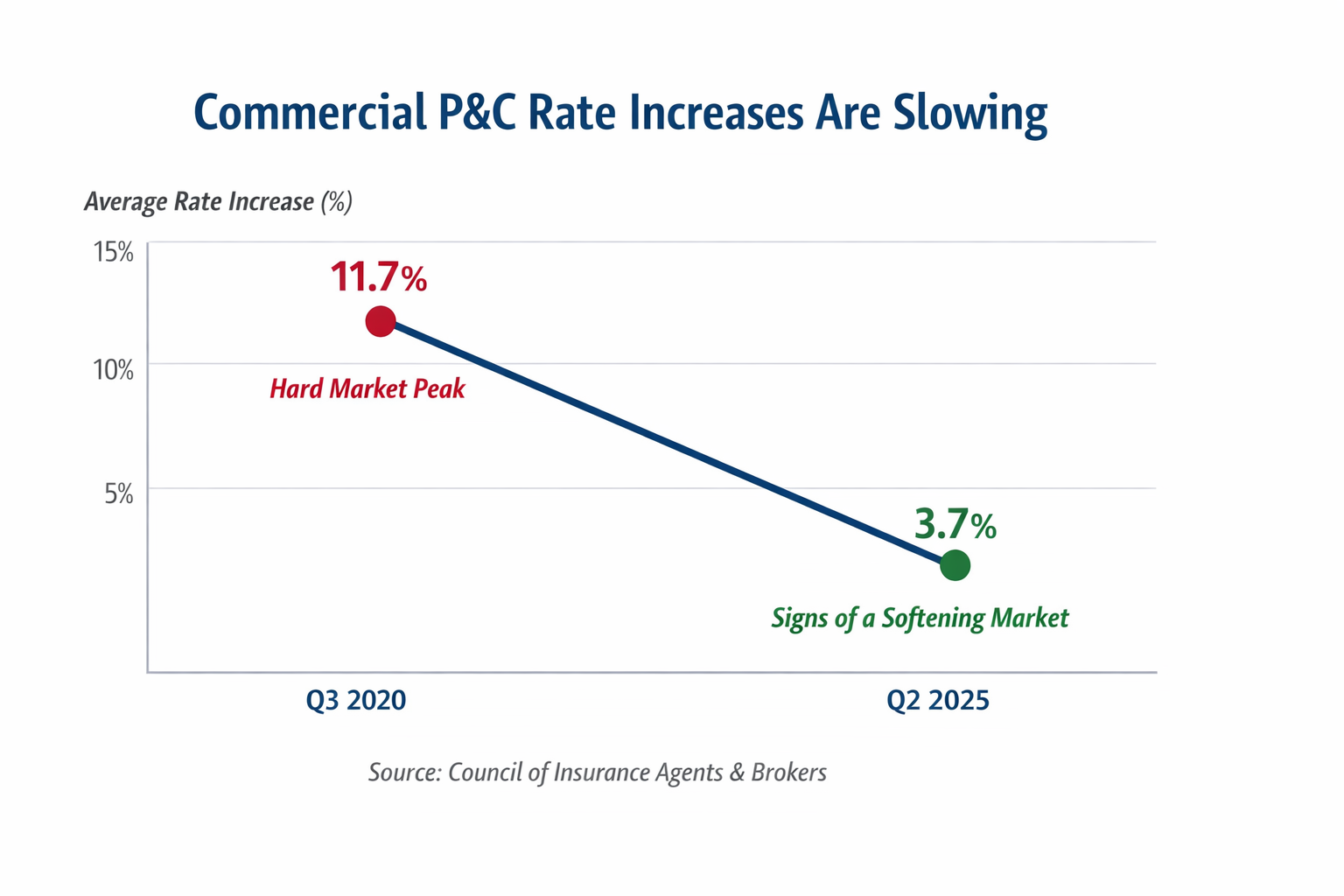

The Council of Insurance Agents & Brokers reports that commercial property and casualty rates increased by an average of 3.7% in the second quarter of 2025. Overall, rates are still rising, and this marks the 31st consecutive quarter of premium increases, but the increases have slowed significantly. For comparison, rates were up by an average of 11.7% in the third quarter of 2020.

Commercial property and casualty rates increased by an average of 3.7% in the second quarter of 2025.

Many individual lines have also exhibited noticeable improvement. In the second quarter of 2025, commercial property rates were up by only 1.9%, a far cry from the double-digit increases seen in 2023. Several lines, including cyber, D&O and employment practices, saw price decreases.

Some lines are still troubled. Umbrella coverage saw the steepest price hikes at 11.5%, a rate hike attributed to nuclear verdicts and litigation trends. Overall, however, the insurance market is becoming more favorable.

What the Softening Market Means for Your Agency

On one hand, the softening market should make coverage placement challenges easier. On the other hand, lower rates could make your job much harder because the competition is going to intensify. Competing agents will be approaching your clients, and at the same time, your clients may be exploring their options to see if more affordable solutions are available.

Lower rates could make your job much harder because the competition is going to intensify.

Six Steps to Take Now

1. Resurrect your tried and proven lead generation practices.

For a few years now, agents have devoted most of their time to finding acceptable, affordable coverage for clients. Basically, agents have been in crisis mode. Now that the market is easing, it’s time to revive the lead generation practices that you used before the hard market.

Take advantage of the insurance shopping frenzy and convince new clients to switch to your agency. This will involve updating prospect lists, cleaning up your CRM system, and evaluating commercial niche marketing. You will also need to train your sales team and set sales quotas that are in line with current conditions.

Also, review your marketing practices. Are you still posting to social media, sending out a client newsletter and sponsoring community events? Do you need a new website or Google Business profile? Now’s the time to build name recognition to support your producers.

Last but not least, establish and track key metrics including your close ratio, customer retention rate, average revenue per client and your quote-to-bind ratio.

2. Revisit client relationship and referral strategies.

To avoid customer churn, you need to proactively retain clients. During the COVID-19 pandemic and the hard market that followed, you may have dialed back your relationship-building practices. Perhaps you used to meet your clients in person, but in recent years, video calls replaced those meetings. Maybe you used to host a client appreciation event every year, but it fell by the wayside. Now, with the market shifting and competition increasing, it’s time to bring these practices back and connect with clients in a more personal, impactful way.

You should also look for opportunities to cultivate referral sources. Reconnect with CPAs, mortgage brokers and other professionals who serve your clients. Encourage your producers and account managers to send out handwritten thank you notes with business cards enclosed.

3. Focus on cross-selling and up-selling.

As carriers offer better terms, you can gain new clients by helping them secure the coverage that was out of reach in the past.

Some customers (especially in the property space) may have skimped on limits to save money. With the market evolving and risks becoming more complex, now is the perfect opportunity to revisit their policies. You can help them secure higher limits or broader terms – often for the same budget or just slightly more to ensure they have the proper coverage when it matters most.

You can also expand your book by cross-selling to your current clients. Cyber insurance for your commercial customers is a great example. Right now, cyber insurance rates are falling, but cyber risks are an increasingly serious threat to businesses. Some of your clients may have gone without cyber coverage in the past because rates were surging. Now that the market has improved, it’s time to take another look at the available coverage options.

4. Refine or rebuild your team.

During the hard market, you may have put off hiring new people or replacing team members who left. The responsibilities of some roles may have morphed over time to meet your agency’s evolving needs. Now it’s time to staff with intention.

Conduct a personnel assessment, reviewing every department’s staffing and workflows. Is anyone overworked? Underworked? Are there backlogs? Are there any tasks that could be better managed by new technology?

There will be a lot of market share up for grabs as policyholders explore their options in a soft insurance market, and with a stronger team, you’ll be in a better position to win their business.

5. Invest in your agency.

Beyond hiring new people and expanding marketing and sales, think about other ways you can invest in your agency to capitalize on growth opportunities.

For example, are you still using old technology? Maybe it’s time to look at new solutions like a Voice AI phone system to ensure your phone is answered 24/7, with English and Spanish language options. Or consider a digital policy renewal workflow to enhance customer retention.

This could also be a good time to think about an acquisition. By acquiring another agency, you can rapidly expand your book, gain new resources and penetrate additional markets. It’s a bold move, but if you’re ready for serious growth, it’s worth considering.

6. Leverage an insurance network.

A network can help you take full advantage of the softening market. If you’re already part of a network, make sure to leverage all the tools and resources available to you, which may include carrier introductions, training, software, back-office support, and acquisition assistance.

If you’re not part of a network yet, consider joining one. Here are some things to consider as you explore your options:

Which markets are available? Many agents join networks for the carrier access, but not all networks provide the same level of access. Make sure you’re getting access to top personal and commercial carriers, including excess and surplus line markets. Also, ask if direct code is a possibility.

Is the contract agent-friendly? Some networks charge excessive fees or place restrictions and requirements that don’t always serve your agency’s best interests. Read the fine print carefully and ensure you’re comfortable with all the terms and obligations.

Is there a commission cap? Find out if commissions are capped when you reach a certain premium volume. As you build your business, that one detail will make a significant difference in your revenue.

Does local support exist? Is there a local state or regional manager to provide guidance? What about marketing, training and networking opportunities?

Does the network have national clout? As you grow your agency, you may want to expand into additional regions or explore new market niches. A large network with national clout can help you do this. It can also lead to stronger carrier relationships, faster support and enhanced earning potential.

Smart Choice provides member agencies with access to more than 120 carriers and 3,000 products, including personal, commercial and excess and surplus markets. We also provide product training as well as sales and marketing support to help agencies grow – and we do all this without any fees. Learn more.

FAQ—As the Market Softens

What does it mean when the insurance market softens?

Right now, the industry shows signs of softening. Overall, the insurance market is becoming more favorable.

How does a softening market impact independent agencies?

On one hand, the softening market should make coverage placement challenges easier. On the other hand, lower rates could make your job much harder because the competition is going to intensify.

What should agencies do first as competition increases?

Resurrect your tried and proven lead generation practices. Take advantage of the insurance shopping frenzy and convince new clients to switch to your agency.

What are key metrics agencies should track right now?

Establish and track key metrics including your close ratio, customer retention rate, average revenue per client and your quote-to-bind ratio.

How can agencies expand revenue in a softer market?

Focus on cross-selling and up-selling. Now that the market has improved, it’s time to take another look at the available coverage options.

How can an insurance network help as the market shifts?

A network can help you take full advantage of the softening market. Make sure to leverage all the tools and resources available to you.